DUBLIN- ДУБЛИН

|

|

Know Whom you are dealing with. You

may wish to decide whether you feel comfortable about our credibility, before you

read our opinions and advice |

Ьетоды снижения налоговых платежей при использовании Российских и иностранных офшорных компаний

| English |

Russian |

|

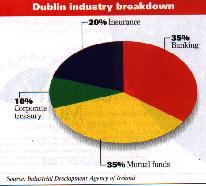

Dublin's membership of the European Union means it offers the advantage of being a tax-efficient centre within Europe. This means that many of the products offered from Dublin also comply with onshore legislation and can be sold by advisers freely without restriction. The disadvantage is that the constant talk of EC tax harmonization is viewed as a threat to its low-tax status. However, judging by the number of providers setting up service operations in Dublin, the threat of tax harmonization is either not taken seriously or seen as an integral reason why advisers should be using the products and services which are on offer. The current impetus for growth in services offered by Dublin providers is viewed as the European 'pensions time bomb'. Lessons have been learned from the US where individuals invest retirement assets in mutual funds chosen by employers. This investment trend is now appearing in Europe, which is showing signs of a growing 'instividual' market. As a result, asset managers must market increasingly to both the individual and to institutions. The costs and fees of funds such pension-based funds, which clearly impact on the net performance available to the investor, are determined by the effectiveness of the fund struc- ture. Implicit within this is the choice of domicile of the fund. Many of the major fund houses are now based in Dublin and include ABN Amro, Barings, Deutsche Morgan Grenfell and HSBC. Qualifying activities A wide range of activities and their ancillary services can qualify for the IFSC (International Financial Services Center in Dublin and are defined by the Finance Act, 1987 and subsequent legislation. These activities can be summarized as follows: These activities must be carried out on behalf of non-Irish residents and in non-Irish currencies. Fiscal Regulations Apart from the favourable corporate tax regulations there are a number of other fiscal incentives pertaining to compa- nies operating in the IFSC including:

Time zone: GMT Location: Ireland is located in Europe to the west of Great Britain. Govermnent contacts: The Central Bank of Ireland |

═ Political Stability: Excellent Bank Secrecy Law: No Ebglish Common Law: Yes Company Type: Exempt Exchange Controls: Nil Offshore Revenue Tax: Nil Owner Disclosure: Not Publicly Language: English Domicile Migaration: Doubtful Offshore Banking: No "Shell Companies: Yes Minimum shareholers 2 Mininum directors: 2 Corproate directors: No Secretary Required: Yes Bearer Shares: No Registered Agent: Yes Local directors: No Diirectors disclosed: Yes Local Meetings: No Trusts: Yes Asset Protection Trust: No Tax Treaties: Australia, Austria, Belgium, Canada, Cyprus, Czech Republic, Denmark, Finland, France, Germany, Hungary, Israel, Italy, Japan, Luxumbourg, Netherlands, New Zealand, Norway, Pakistan, Poland, Portugal, Russia, South Africa, South Korea, Spain, Sweden, Switzerland, UK, USA, Zambia |

Translation into Russian pending. |

Palms & Company, Inc. Copyright 1998

|

Palms' click image to return to:

|

═

CAN

YOU REALLY RELY UPON PALMS & COMPANY?

You are One of the ![]() Who can.

(World Population Counter)

Who can.

(World Population Counter)

|

|

No,

we don't need Palms.

|

Attention Brokers, Agents , Intermediaries, Mandates of Principals/Buyers

Go to TOP of this page

RETURN

TO HOME PAGE

RETURN

TO HOME PAGE

═

═

═

═

═

Awards

Awards

Can

Palms deliver?

Can

Palms deliver?  What is their

track-record ?

What is their

track-record ?

O.K.

get a hold of Palms

O.K.

get a hold of Palms{kind=link}